In today’s fast-paced financial landscape, managing unexpected expenses or bridging the gap between paychecks can be challenging. Cash now pay later loans—often referred to as Buy Now, Pay Later (BNPL) or short-term installment loans—have emerged as a flexible solution for consumers needing immediate access to goods or funds. This overview explores the mechanics, advantages, and necessary precautions associated with these modern lending options.

What Are Pay Later Loans?

Pay later loans are financial arrangements that allow consumers to make purchases or access funds immediately while deferring the actual payment to a later date. Unlike traditional credit cards which revolve indefinitely, these loans are typically structured as installment plans with a clear end date. They are widely used for retail purchases, but the concept also extends to cash loans for services.

For example, if a homeowner faces a critical plumbing failure costing $3,000, they might not have the liquidity to pay upfront. In this scenario, a 3000 emergency loan structured as a pay-later installment plan allows the work to be completed immediately, with the homeowner repaying the amount in fixed bi-weekly or monthly chunks. These loans can range from small retail purchases of $50 up to larger personal loans of several thousand dollars, depending on the lender and the borrower’s creditworthiness.

Financial Flexibility: Discover How Pay Later Loans Work

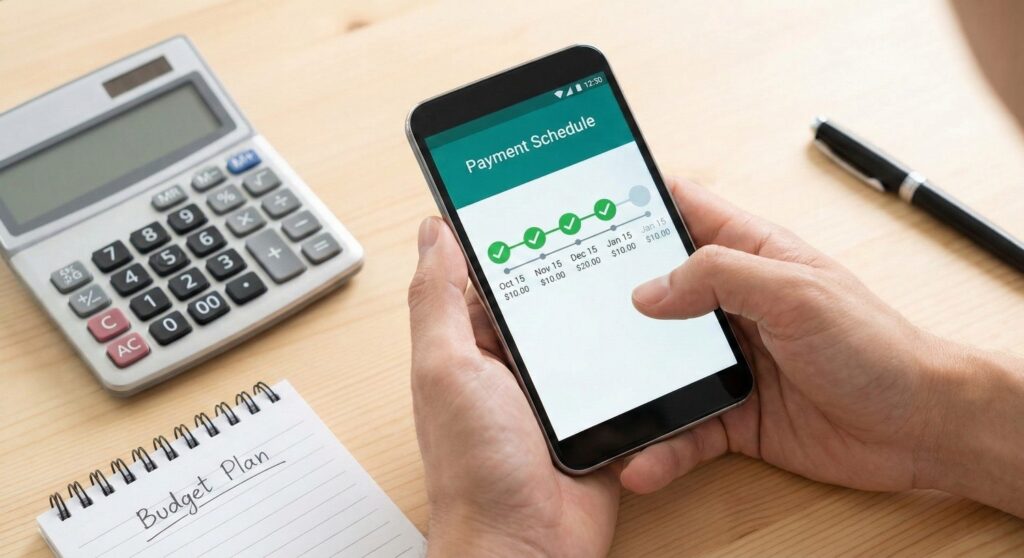

The mechanics of these loans are designed for speed and simplicity. When you decide to apply for urgent loan options or use a BNPL service at checkout, the process is typically digital and instantaneous.

- Application: The borrower provides basic personal details (name, address, date of birth) and payment info.

- Soft Credit Check: Most pay later services perform a “soft” credit pull, which does not impact your credit score. This makes them accessible to a wider range of people compared to traditional bank loans.

- Repayment Schedule: Once approved, you receive a clear schedule. A common model is the “Pay in 4” structure, where 25% is paid upfront, and the remaining three payments are deducted automatically every two weeks. Longer-term loans may stretch from 3 to 24 months with interest.

Advantages of Pay Later Loans

One of the primary benefits of this lending model is accessibility. For someone thinking, “I need loan approval quickly to cover a medical co-pay,” the speed of automated approval is invaluable.

- Interest-Free Options: Many short-term BNPL plans (typically those paid off in 6 weeks or less) charge 0% interest, provided payments are on time.

- Budget Management: By breaking a large lump sum into smaller, predictable payments, consumers can manage cash flow better without draining their savings entirely.

- Credit Building: Some longer-term pay later lenders report repayment history to credit bureaus. Consistently paying on time can help build a positive credit profile.

Potential Risks to Consider

Despite their convenience, these loans carry risks that borrowers must understand to avoid debt traps.

- Fees and Interest: While short terms may be free, missing a payment often incurs late fees, typically ranging from $7 to $10 per missed installment. Longer-term financing can carry Annual Percentage Rates (APRs) ranging from 10% to 30% or more, making the purchase significantly more expensive.

- Overspending: The ease of clicking “pay later” can lead to impulse buying. If a consumer stacks multiple loan payments simultaneously, the total monthly obligation can quickly become unmanageable.

- Credit Damage: While applying might not hurt your score, defaulting on payments almost certainly will. Lenders may send unpaid debts to collections, which drastically lowers credit scores.

How to Use Pay Later Loans Responsibly

To maximize the benefits while minimizing the risks, borrowers should adopt a disciplined approach.

- Set a Budget: Before you apply, calculate your monthly disposable income to ensure you can absorb the new payment.

- Read the Fine Print: Understand the specific APR and late fee structure. For a 3000 emergency loan, even a small difference in interest rate can add hundreds of dollars to the total repayment cost.

- Track Due Dates: Set up autopay or calendar alerts. Since these loans often rely on bi-weekly schedules (matching typical pay cycles), they may not align with your monthly bill-paying routine.

Conclusion: Navigating Pay Later Loans Wisely

Pay later loans offer a modern, efficient way to handle expenses, providing a buffer when liquid cash is tight. By understanding the specific terms—whether it’s a 0% interest retail plan or an interest-bearing cash now pay later loan—you can leverage this tool to maintain financial stability during emergencies. As with all debt, the key lies in responsible usage: borrowing only what you can afford to repay and adhering strictly to the schedule to avoid unnecessary costs.